Most investors frame Google’s AI story around Gemini, Search, and Cloud. That misses the real asset: DeepMind as a research engine that’s betting on what comes after the current transformer wave.

The market may be underpricing Google’s ability to win the next architectural shift in AI — not just defend its position in the current one.

This analysis started with a video — Pourya Kordi’s DeepMind Was Two Steps Ahead, AGAIN!, which walks through the non-transformer bets DeepMind is making. Worth watching before reading on:

The Core Investor Question

Is Google merely keeping up in AI, or is it building the infrastructure for the next paradigm entirely?

Benchmark wins and flashy demos are noise. The real question is whether Google is accumulating research optionality — the ability to pivot and lead if the current dominant AI architecture hits a wall.

DeepMind is Google’s answer to that question.

What DeepMind Is Actually Working On

DeepMind is not making a single bet on one architecture. It’s running a portfolio of bets on what comes beyond standard transformers:

- Recurrent memory models and hybrid architectures — bringing smarter recurrence back to solve context and efficiency problems

- Diffusion-style language generation — parallel generation rather than token-by-token prediction

- Multimodal world models — reasoning through simulation and grounded understanding of the physical world, not just text patterns

- Hybrid attention/recurrent systems — incremental evolution from today’s architecture toward something more efficient

DeepMind appears to be challenging four assumptions simultaneously: that transformer attention is the final architecture, that autoregressive generation is the final decoding method, that bigger context windows are the best memory solution, and that text prediction alone gets you to AGI.

Why Move Beyond Transformers at All?

Transformers are dominant for good reasons — they scale, they perform, and the ecosystem around them is massive. But they have real structural weaknesses:

- Inference cost is brutal at scale

- Memory load grows with context length

- Context inefficiency — long context windows are expensive to build and expensive to run

- Token-by-token generation is fragile and computationally wasteful

The next leap in AI capability may not come from adding more GPUs to today’s transformer stack. It may come from a fundamentally more efficient architecture. If that happens, the lab that already did the research wins.

The Most Important Directions

Recurrent/hybrid memory models are the most credible near-term threat to plain transformer dominance. They attack the inference cost and context problems directly. If a hybrid model matches transformer quality at materially lower inference cost, that’s not a research win — that’s margin.

Diffusion language models are interesting but farther out. Parallel generation and better editing/infill capabilities could be significant, but the path to production isn’t as clear.

World models are the biggest moonshot and the hardest to copy. It’s not just model architecture — it’s data, objectives, product framing, and research culture. Google has YouTube-scale video data, DeepMind’s simulation research heritage, and the patience to pursue it. Most competitors are still shipping chatbots.

What This Could Mean for Google’s Business

If any of these directions converts from paper to product, the implications compound:

- Better model economics could improve margins across AI products and Cloud

- More efficient inference matters enormously at Google’s scale — small per-query improvements multiply across billions of requests

- Stronger multimodal AI reinforces Search, Workspace, YouTube, Android, and Cloud simultaneously

- DeepMind breakthroughs in production would convert research into operating leverage — the kind that shows up in earnings

The most direct read-through is Google Cloud. AI demand is already pushing enterprise customers toward infrastructure-heavy platforms. If Google can pair TPUs + proprietary models + DeepMind breakthroughs, Cloud’s strategic value compounds. Cloud growth is likely the first place investors see the payoff from DeepMind’s work.

The Bull Case

Google has something its competitors don’t fully match at once: frontier research depth, unique data at scale (Search, YouTube, Maps, Android), custom silicon (TPUs), global distribution, and the capital to fund long-horizon bets.

DeepMind gives Google architectural optionality in case transformers top out. If the next winning AI stack looks different from today’s, Google may be better positioned than the market currently assumes. The prior DCF work we ran on GOOG pegged fair value at $554–708 (midpoint $632) — that analysis didn’t fully price in what a DeepMind-driven architecture advantage could mean for Cloud margins and AI product monetization.

The Bear Case

Google has a long and well-documented history of brilliant research with uneven commercialization. The bottleneck has never been the science. It’s been turning lab wins into market wins before the window closes.

The other risk: architecture ideas in AI leak fast. Papers are basically invitations to copy. If Google proves a recurrent/hybrid model works at scale, OpenAI and Anthropic can probably replicate the broad idea in 6–18 months. They’re not blocked by talent — they’re blocked by inertia, product commitments, and infrastructure lock-in. That lock-in buys Google time, not permanent exclusivity.

Antitrust still hangs over the core business. The DOJ search distribution case puts roughly $20B per year (the Apple search deal) at risk. And AI search disruption — Perplexity, ChatGPT web browsing — is a slow-burn risk to the 90% search share that funds everything else.

What Investors Should Watch

- Evidence that DeepMind architectures move from papers into Gemini products in production — not just research announcements

- Changes in model efficiency, latency, and inference cost in Google’s AI offerings

- Google Cloud growth rate — Q2 earnings July 23 is the next major checkpoint; 40%+ growth validates the AI infrastructure thesis

- Whether competitors start adopting similar architectures — that’s usually the clearest signal that the research worked

- AI Overviews monetization and Workspace AI performance, which are the near-term commercial proving grounds for Google’s AI stack

Bottom Line

DeepMind is not an R&D trophy — it’s Google’s hedge against AI commoditization.

The market prices Google primarily as a Search and Cloud company that happens to have good AI. The more accurate frame might be: Google is one of the few companies that could win the next paradigm shift in AI, not just the current one.

The key question is not whether DeepMind is brilliant. It obviously is. The key question is whether Google can turn research into product and profit before rivals catch up. That’s where it has historically been inconsistent. That’s also where the upside lives if it gets it right.

Strategically bullish. Near-term, it has to show up in execution.

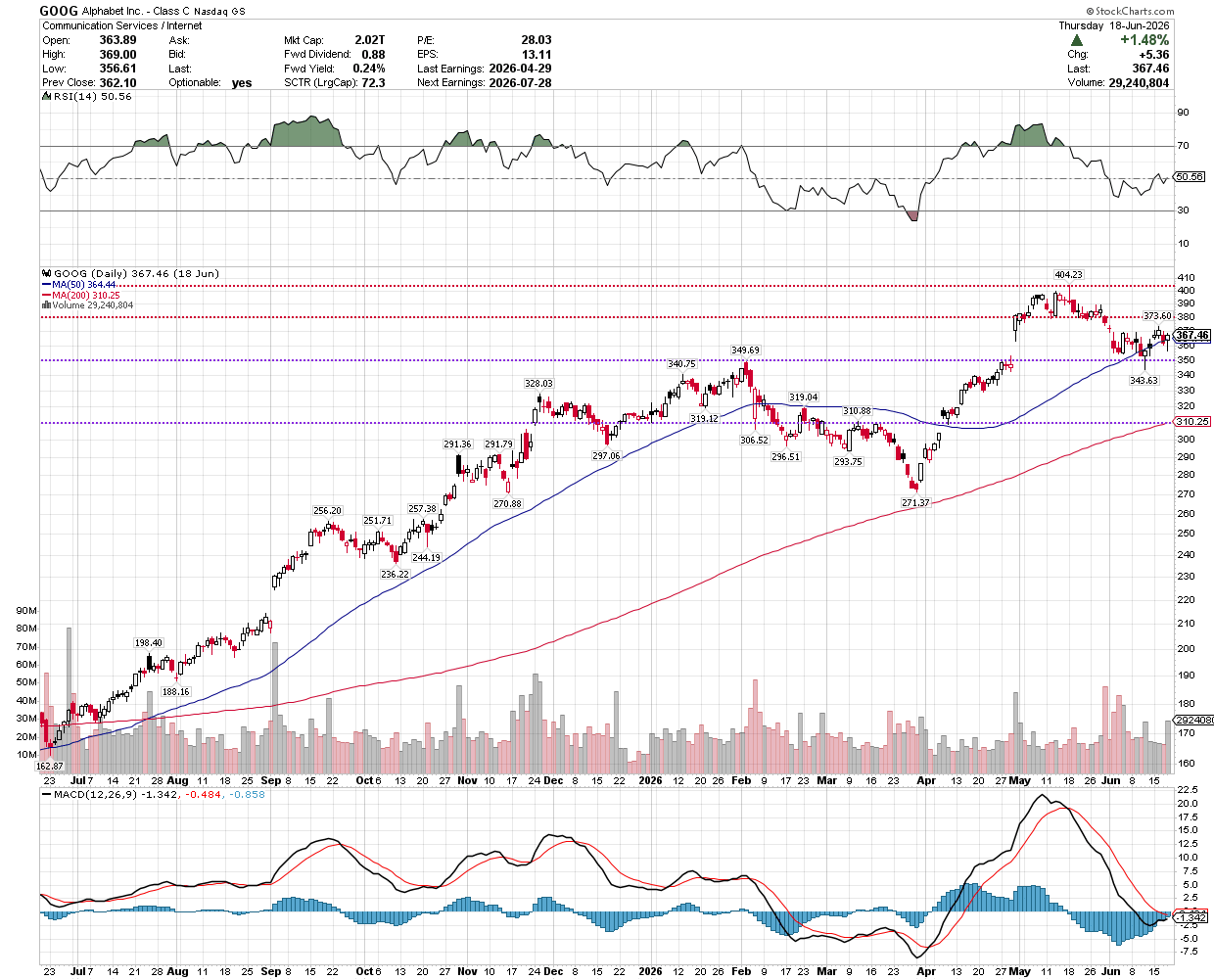

Where GOOG Trades Today

The strategic case has to meet the stock somewhere. GOOG is at $367.46 — about 9% below its February 2026 all-time high of $404, and 18.5% above its 200-day moving average ($310). It’s a pullback inside a long-term uptrend, currently sitting right on its 50-day moving average.

Key levels:

- $404 — 52-week high / ATH (Feb 2026); major overhead resistance

- $380–385 — May 2026 recovery ceiling

- $364 — 50 DMA; the critical near-term inflection

- $349–350 — December 2025 consolidation floor

- $310–315 — 200 DMA; major structural support

A healthy retest of the recovery. Hold the 50 DMA this week and the next leg targets $380–385; lose it and $349 is the first real floor. RSI is neutral at ~51 and MACD’s bearish momentum is decelerating — the pullback looks like it’s losing steam.

GOOG trades at $367.46 as of this writing, approximately 9% below its February 2026 ATH of $404, and 18.5% above its 200-day moving average of $310. Q2 earnings are July 23, 2026. Cloud growth rate is the single most important number to watch.

Not financial advice. Do your own due diligence.